Who is charging a x100 markup for electronic payments processing?

Bang, Bang. I am not Pomp but I am sure he wouldn’t mind me borrowing his opening to discuss why American Big Banks are ripe for disintermediation in their electronic payment processing businesses for 3rd parties.

The US payment system is undoubtedly behind (itself, the UK payment system and the Chinese payment system).

Admittedly, the US ACH payment system which currently handles electronic payments has grown while America awaits FedNow, planned to launch next year.

Meet NACHA which governs the growing ACH Network for depositary institutions, as an administrator and industry trade association. US payment Fintechs to date are not part of this network and have to processes their transactions through US depositary institutions.

ACH`s rosy growth

The volume of transactions that ACH processes has been growing consistently over the past 7 years. According to Bloomberg, the increase is more than 1 billion transactions per year.

Nacha reports that in 2021, the top 50 US banks originated around 25 Billion of ACH transactions. This figure does not include electronic transactions in which the originating bank and the receiving bank are the same, and therefore, the gross amount is actually larger.

This 25 Billion transactions represents an 8.2% increase from 2020. These top 50 banks account for 92.1% volume of ACH transactions. Total ACH transactions were around 29 Billion and were worth around $73 Trillion!

A typical ACH electronic transaction takes 48 hours (some do take 3–4 business days). Same day ACH transactions are still very rare. Bloomberg reports that they accounted for c. 600 million in 2021, an increase of 74%, but still a dismall 2.4% of the 25 billion ACH transactions.

ACH`s rising systemic risk

The Nacha detailed figures for the top 50 US banks show an alarming concentration.

Two US banks originated around 50% of ACH transactions in 2021.

Wells Fargo originated 7.7 Billion ACH transactions

JP Morgan originates 5.1 Billion ACH transactions

The irony is that the growing ecosystem of payment Fintechs are obliged to process their transactions through these banks, as they continue to be denied access to the Fed. The rationale being risk management issues.

So, we are fooled to think that payment services competition in the US is growing with all these Fintechs but behind the scenes there is increased systemic risk with two Big Banks handling 50% of the ACH payment transaction volume.

WISE, wisely argues these points in their latest April letter to the Federal Reserve (link here).

The eye opener of the WISE comments to the Board of Governors of the Federal Reserve, was around the fees that are charged by these banks.

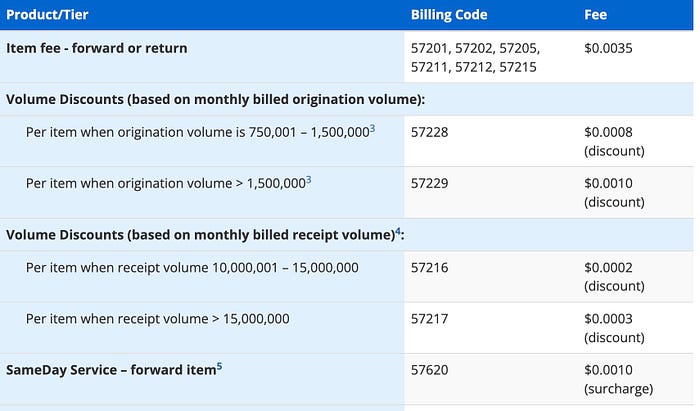

The privileged US Banks that have direct access to the Fed are paying fees to the Fed that are at most $0.0035.

The Wells Fargos of the Americas then turn around and charge payment Fintechs as much as x100 times that Fed fees — Wise claims fees around $0.35!

Instant payments with fee transparency are needed. But most importantly, a more distributed payment processing network is needed. Ironically, as the number of `Fintech` payment providers has increased, the US payment system is increasing the concentration risk behind the scenes.

We are in the second decade of the 21st century, and any payment processing design (behind the scenes) needs to have fee transparency and distributed points of failure.

Big US Banks are overcharging the entire payment `Fintech` ecosystem that have largely contributed to the increase of electronic payments. Disintermediation of this is coming. Their increasing concentration risk in the US banking system behind the scenes, needs to be called out.

Caitlin Long, founder and CEO of Custodia Bank (I have so much difficulty with remembering to use their rebranding — I still think of them as Avanti), strongly believes in the disintermediation potential of the Lightning Network on the Bitcoin Blockchain. I recommend listening to her as she understands payments and Bitcoin extremely well and is consistently courageous and calls out the crypto community often. I spotted the WISE letter to the Fed from Caitlin`s feed.

“Surround yourself with people you can always learn something from and work with people that are better at their craft than you are.”

📌 Twitter: https://twitter.com/efipm

📌 Subscribe to my YouTube Channel with my insights and industry leader interviews. New video every Wednesday: https://www.youtube.com/EfiPylarinou

📌 Spotify Podcasts. Follow here: https://open.spotify.com/show/5bRkZEYHSwPiGx7vTqylw6?si=Mg3hN5PDQ86K10GjeK52jw

📌 Linkedin: https://www.linkedin.com/in/efipylarinou/

📌 Web: https://efipylarinou.com/