Build Wallets for Women

There are several financial services providers that have focused on women and designed female-focused financial services, but not enough. The range of female-focused financial services aims to tackle women`s low conversion rate, all the way to leveraging data and better understanding women`s financial health challenges.

It is clear that female physical and mental health issues are different than male physical and mental health issues. Similarly, female financial wellness issues differ from male financial wellness issues.

There are several explanations for these differences. The bottom line is that there are major gender gaps even within the innovative Fintech ecosystem which is no longer at its early stages. I was actually struck by the Fintech female gender gap reported in the recent report `Fintechs serving the Female economy` by the Financial Alliance for Women, in collaboration with Finstep Asia and the Global Fintech Fest. Only 27.6% of women use Fintech financial services and this gender gap apparently is wider than the gap for bank account ownership and of course wider than smartphone ownership and mobile internet usage.

This means that Fintechs despite their improved accessibility, better customer experience, and ability to personalize services based on data, have not yet managed to change the Finserv gender gap stats.

`Country characteristics and several individual-level controls explain about a third of the unconditional gap. Gender differences in the willingness to use new financial technology or fintech entrants if they offer cheaper services account for over half of the remaining gap.` Fintech Gender Gap paper by BIS

There is therefore an opportunity to serve more women. If we look at the projections around spending alone:

Women will control 75% of the world’s discretionary spend in 5yrs (2028)

I cannot help but think that Fintechs have to build the wallets that these women will use!

Build wallets for Women

Whether you are thinking about the functionalities women need more than men, or designing your rewards strategy that appeals to women, or the customer experiences women prefer; you need to build Operating systems with Women in mind.

If you believe that Wallets will be the dominant Operating systems for our financial lives and financial health, then build wallets for women. If you are a niche Fintech provider that can and will partner with a Financial Operating system provider, then again design your financial product with women in mind.

Currently, Fintech services for women are standalone and without a significant variety. More importantly, we are in the early stages of the Open Finance trend (Open banking and lending are leading and open wealth and insurance are behind) and female-focused financial services cannot escape this. The Fintech gender gap for female services will only start closing when the scattered female fintech services are integrated and or embedded.

Ellevest, is a seasoned female Fintech focused on investing since 2014. They just published an alarming report showing that women’s financial health is at a five-year low. This index is US focused and looks at factors like pay gap, retirement gaps etc. Fintech needs to come to the rescue of this awful reality.

In the UK, women’s pensions are £100,000 less than men`s and there is a £15 billion gender investment gap. Vestpod and Smart Purse are both helping women narrow this gap with similar services that Ellevest provides in the US.

All three are a mixture of PFM (personal financial management), WealthTech (investing), coaching and community building.

In the EU, FinMarie out of Germany is offering similar services for women. Their app enables e-learning communities, offers robo-advisor type investment capabilities and more traditional financial coaching in real estate and business management.

Cashmere’s digital wallet is a Fintech helping women save for luxury items with a mantra ` FOR SMART WOMEN WHO ARE IN CONTROL OF THEIR LIVES, WARDROBES — AND WALLETs`.

SavewithCashmere is enabled by Mangopay a B2B payments Fintech and part of the French charity crowdfunding platform, Leetchi and Credit Mutuel Arkéa, the French banking group.

In 2020, the female-focused Fintech HerMoney was launched in Brazil with the motto `Your financial Whatsapp!`. Their focus is to help women entrepreneurs with financial management services like mentoring, educational content, financial reports, and integration with key financial institutions so that they can grow their businesses. HerMoney is partnering with microfinance institutions to offer credit lines to women entrepreneurs.

The Brazilian Fintech is unrelated with HerMoney, the US digital media company focused on improving the relationships women have with money founded by Jean Chatzky, a financial editor of NBC’s “Today” show.

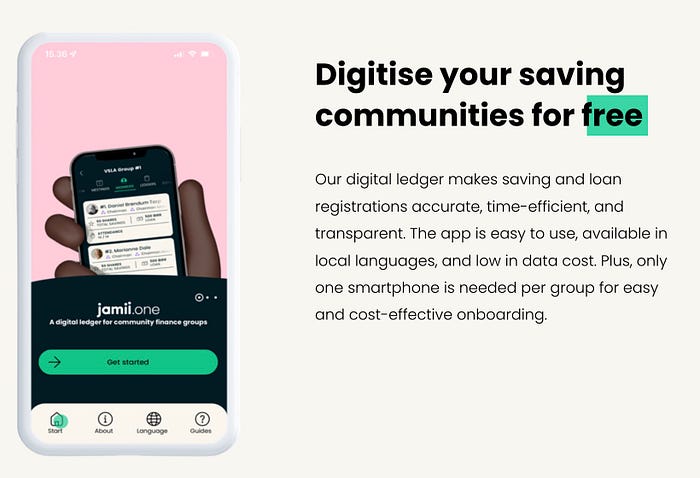

In Africa, Jamii.one is a Fintech focused on providing access to credit for women (not only) for now in Kenya and Ethiopia. The digital tool enables local women’s savings groups build their credit by keeping an accurate and secure record of their savings and loan activity. Women don’t even need to have a smartphone or formal identification because the group takes care of it.

In India, Upwards is a fintech startup offering a broad variety of instant personal loans exclusively for working women professionals.

The bottom line is thatwomen`s financial wellness is not taken care of. This is an opportunity for Fintechs to create a financial operating system for women. If you believe in the potential of Wallets becoming the core of a financial operating system, then build Wallets for women.

I am puzzled that neobanks and other consumer-facing Fintechs are not targeting women. The only mention of a bank with a female-focused offering integrated into their e-banking that I came across, was a Swiss traditional bank, Bank Cler that launched in 2001 Eva, an offering designed especially for women. Eva provides private female customers with consulting services and access to networking and events. However, this service has been shut down.

Let me know in the comments if there are neobanks with a female-focused offering.

The only area that has more services is the investment area, as there are many investment clubs for women globally (however, this is not because of Fintech). Also, crowdfunding platforms seem to be attracting capital for women entrepreneurs at a considerably higher rate than VCs.

📌 Twitter: https://twitter.com/efipm

📌 Subscribe to my YouTube Channel with my insights and industry leader interviews. New video every Wednesday: https://www.youtube.com/EfiPylarinou

📌 Spotify Podcasts. Follow here: https://open.spotify.com/show/5bRkZEYHSwPiGx7vTqylw6?si=Mg3hN5PDQ86K10GjeK52jw

📌 Linkedin: https://www.linkedin.com/in/efipylarinou/

📌 TikTok: https://www.tiktok.com/@efiglobal

📌 Web: https://efipylarinou.com/